In the early ’70s, an anonymous source, “Deep Throat,” gave two Washington Post reporters a hint that would crack the case of the mysterious break-in at the Democratic National Committee headquarters. The clue? “Follow the money.” Not only did the clue lead to President Nixon’s resignation, but it also coined a term that has since been useful for analyzing market dynamics in different industries — edtech included.

For more than three months, the EdSurge team has analyzed the money trail in the US K-12 edtech industry. The team focused on these questions: Who are the investors? Where is their money going? And what are the returns so far?

In “How Money Shapes Tools and Schools,” EdSurge reveals that from 2010 to 2015, $2.3 billion was invested in the US K-12 edtech industry. Six years into this phase of education technology, investors and entrepreneurs are more savvy and circumspect about how capital is shaping the companies and products in our schools, as are the millions of students and teachers using these tools. They know there’s far more than dollars at stake here; when an edtech company goes bust, the hopes and spirits of teachers and students fizzle, too.

Press releases proclaim lofty goals and flashy dollar amounts, while news stories declare the booms and busts of the sector. It can be difficult to parse the truth from the myths So EdSurge gave it a go. Here’s what we’ve found with five years’ worth of research and data:

1. There really isn’t any money in the edtech industry.

Myth.

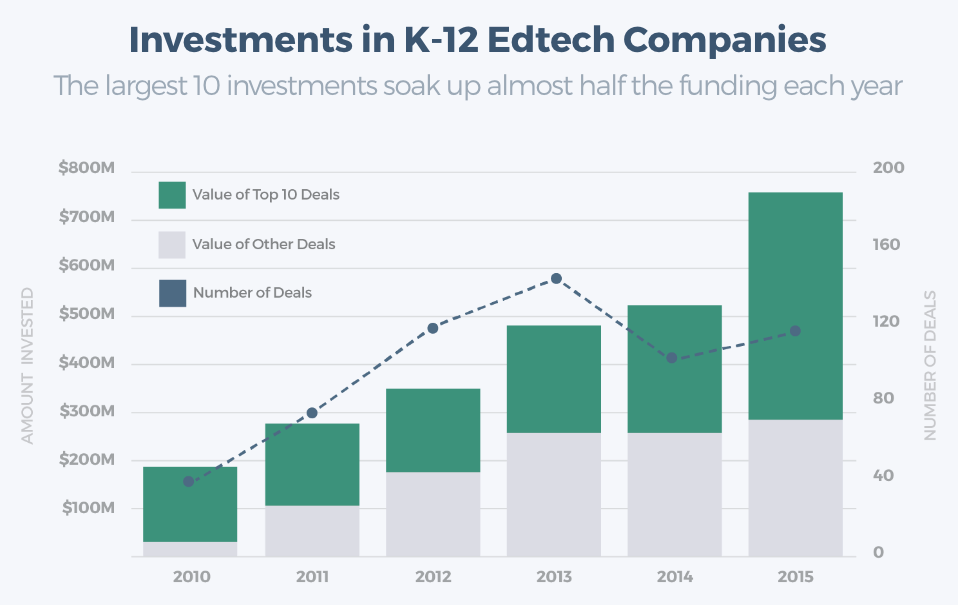

$2.3 billion, 558 deals. Those numbers quantify the “dollars and deals” invested in US K-12 edtech companies from 2010 to 2015. There has been more money invested in US K-12 edtech companies in the last six years than ever before, and it has grown consistently year over year.

The evidence that there is money — and interest — in the edtech industry does not stop in absolute dollar amounts. There have also been more players in the sectors: The number of investors, as well as the quantity of companies receiving investment, has been growing. Since 2011, 14 accelerator programs with a focus on edtech have been created.

2. Investors focus only on the bottom line.

Myth.

Yes, investors do have money on their minds. But there are other factors at play, too. Angels, incubators and mission-aligned investors have supported many of edtech’s early-stage investments.

More recently, the sector has also seen the rise of a new type of investment organization, one that focuses on “social mission” even as it watches the bottom line. These organizations typically specialize in education or have verticals devoted to education. That makes them more demanding than other investors — they want financial strength and evidence of social impact.

“Sometimes there’s a misconception that if you’re doing impact, you’re not focused on returns. We believe that you can do both,” said Brian Dixon, partner at Kapor Capital, a fund that in 2015 pledged to invest $40 million over the next three years to spur diversity in tech entrepreneurship.

3. There are a few edtech startup “darlings.”

Truth.

One thing is clear: Investors seem to favor a mighty few. Each year, the top 10 deals tend to account for about half the year’s edtech funding. Across the last six years, about 15% of the companies (50 total) have attracted 75% of the investment dollars. This phenomenon is not unique to edtech; biotech is similarly lumpy. Still, many of the companies that have raked in the most funding over the last six years operate beyond just public K-12: Knewton and Chegg also draw revenue from higher education, while AltSchool (whose $100 million Series B round was the largest K-12 deal of 2015) is developing technology in a private school system

4. Edtech startups get less investment than other tech companies.

Truth.

Edtech companies receive leaner support from their backers than their tech counterparts — and they’re doing more with less. Data from analyst firm CB Insights put the median seed deal for technology companies in 2015 at around $1.4 million, while EdSurge’s data suggest edtech seed rounds were closer to $900,000. This trend holds in the Series A round, where the median size in 2015 was about $5.4 million, compared with just $4 million in the K-12 education companies we track.

5. Are you a new company? Forget about it, only the big boys are funded.

Myth.

Edtech has been squarely in the “build” stage, with most funding concentrated at the seed and early stages. For instance, in 2015, seed companies accounted for about half of US K-12 education deals, compared with less than 30% across all venture capital.

6. Winter is coming — at least where funding is concerned.

Truth.

Yes, it’s getting harder to raise money. Early-stage fundraising seems to be slowing down, thanks to increased expectations from investors, competition among startups and the broader investment climate. K-12 edtech companies that raised Series A rounds in 2015 took a median of 540 days to move from seed/angel funding to that early-stage round, which is at least 150 days (or five months) slower than in past years. As investors tighten their belts, edtech companies will need to cut costs and boost revenue to avoid failure.

This EdSurge-contributed article first published in SmartReport on ISTE 2016.

Jessica Zhao leads R&D projects at EdSurge, where she helped launch the “State of Edtech” initiative. She previously led strategy efforts at College Track and started her career as a management consultant at Monitor Deloitte, where she advised Fortune 500, nonprofit and government clients on how to innovate and scale.

__________________________________________

Like this article? Sign up for SmartBrief on EdTech to get news like this in your inbox, or check out all of SmartBrief’s education newsletters, covering career and technical education, educational leadership, math education and more.